- OptimistiCallie

- Posts

- ✂️ Rate cuts are coming

Hey hey, happy Monday!

The headlines are pretty bleak right now, so why not start your Monday off with a dose of optimism?

Before we get there…some not-so-bleak headlines I made last week! OptimistiCallie was featured in Bloomberg and MarketWatch. I also joined Yahoo Finance to talk about how rate cuts could change the calculus for markets (which is what we’ll dig into today).

Wanna spread the optimism? Share OptimistiCallie with a friend😊

Wall Street can’t stop talking about interest rates.

How high they’ve climbed, and how low they could go in the coming months.

The burning question, though, has been about when that first interest rate cut will happen.

Finally, we might have our answer. After a third-straight month of chill inflation data came out last week, markets now overwhelmingly believe we’ll get a rate cut in September. And frankly, I agree.

On paper, one rate cut isn’t a big deal. The prospect for a low-rate world, though, has already sent shockwaves through markets.

The basics

Let’s begin with a primer on the Fed and interest rates. Both topics can get complicated quickly, so I’ll unpack both here. Skip to the next section if you’re looking for my insights – you won’t offend me.

Rate talk can get nerdy quickly. Yield curve inversion, term premium, bond laddering…it’s like a ball pit for textbook-touting know-it-alls.

But let's not get into that. Ninety percent of it is Wall Street trader jargon that doesn’t affect everyday folks like you and me. What matters are the basics: how interest rates are set and how they impact your financial decisions.

Many of us know that interest rates are what you pay to borrow money. Or, what people (or banks) pay you to borrow your money.

Few understand that a small group of academics in DC has a big hand in setting these rates.

I’m talking about the Federal Reserve. The Fed exists to balance the economy through interest rates and other nifty tools in order to keep Americans employed and able to afford things.

The Fed’s biggest tool is the Federal funds rate – the rate banks pay to borrow overnight from other banks. They adjust this main rate through cuts and hikes to either stimulate or cool down the economy.

Here’s how it works.

A lower Fed rate typically means cheaper loans across the board. And when borrowing money is easy and cheap, you’re less incentivized to save and more willing to spend and invest. The increase in spending juices the economy, boosts innovation and lifts spirits.

Everybody is happy…until the pot boils over.

That boiling point was 2021. The economy was running too well, to the point where prices were rising quickly, and everyday things were becoming unaffordable. In response, the Fed started raising its main rate in March 2022, eventually pushing the rate from zero to a blistering 5%.

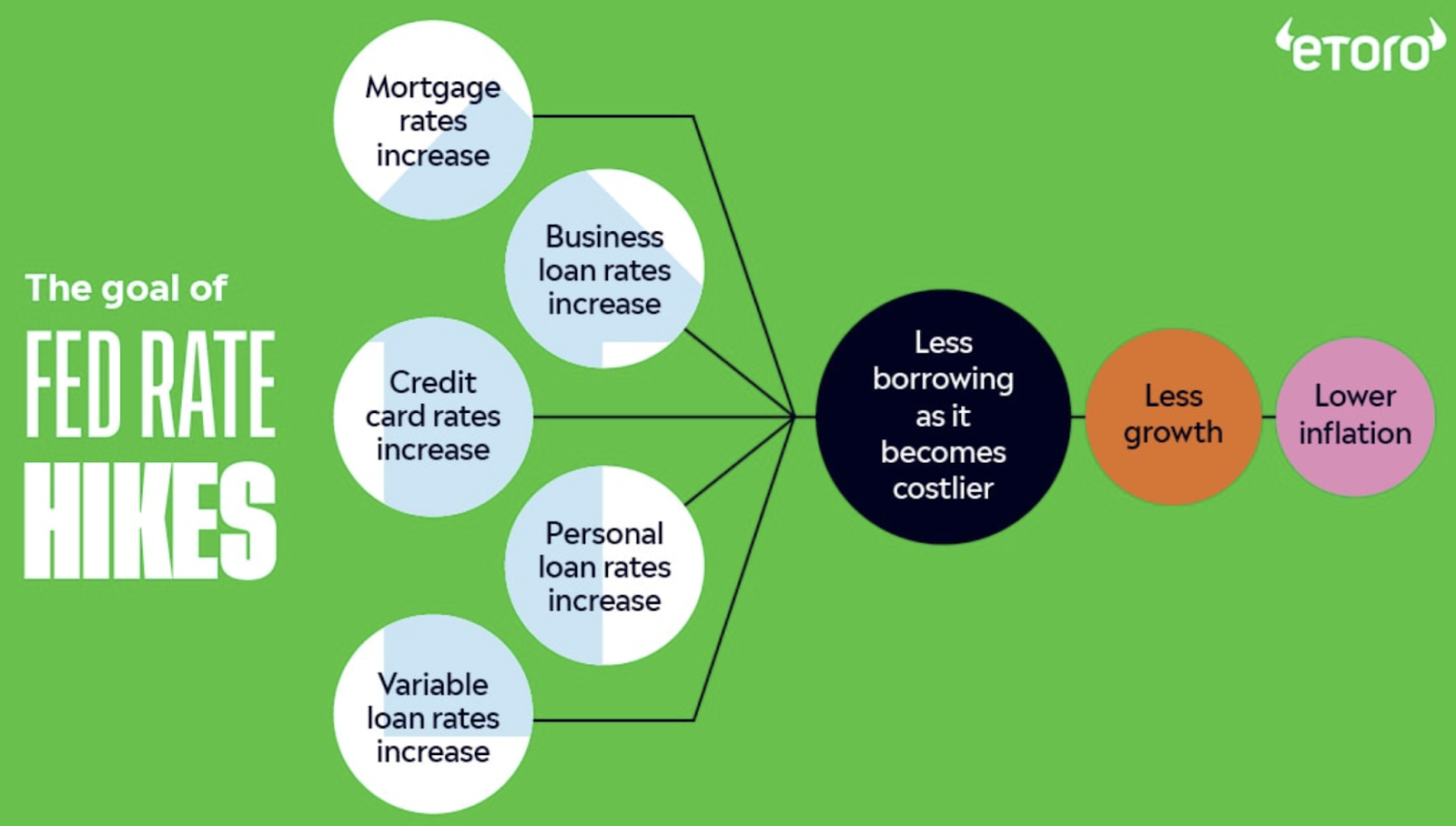

This is how the Fed’s hikes flowed through the economy (h/t to my former eToro colleagues):

It was painful, but necessary. Stock prices dropped, mortgage rates soared to 8%, spending slowed, businesses closed, layoffs surged, and the vibes were just generally off. But hey, at least we got hefty rates on our savings accounts (that a lot of you clearly took advantage of).

In summary: Americans spent less and saved more, which helped inflation slow down to pre-COVID levels.

The Fed was a mastermind, and it was all by design.

So, about that rate cut…

It’s looking like the first rate cut will be tiny. Bond markets expect the Fed to lower rates by 25 basis points – about one-twentieth of the amount they’ve increased rates by over the past two years.

Yet the significance of the first cut goes far beyond its size. That’s why Wall Street won’t shut up about it.

On a basic level, it’d be the Fed’s acknowledgment that our long national inflation nightmare is over. Mortgage rates may not go back to 3% like they were in 2021, but it’s unlikely they’ll stay at a scorching 7% for much longer. Businesses could make strategic decisions better knowing that money is easier and cheaper to raise. Over time, the switch in vibes from despair to hope could usher in a new financial era.

We’ve already seen a sneak peek of that new era in the stock market. After Thursday’s inflation report came out, 80% of S&P 500 members rose on the day. Smaller stocks, which have been especially burdened by higher rates, posted their best day in eight months. The S&P 500 – that gauge of America’s 500 largest companies – actually fell on the day, but the losses were a function of people making different choices with their money (instead of selling out and running for the hills). People were selling Nvidia and piling into real estate trusts and power companies like they were going out of style.

Of course, Thursday was painful if you were heavily invested in tech. But one of the stock market’s biggest critiques this year has been that a few stocks have driven massive gains. Now, more stocks are pitching in, and the foundation of the rally looks stronger.

Interest rates are a major driver of our financial decisions, and the expectation of lower rates could influence so much around us.

Now, I’d be a dishonest nerd if I didn’t tell you about what could go wrong.

And honestly, a lot has gone wrong during rate cuts in the past.

The last few times the Fed cut rates was in response to scary events like COVID and the financial crisis. Stocks ended up falling further after the first cut, before eventually recovering.

The Fed could go overboard, too. The thought of lower rates could turbocharge markets and bring back the go-go everything is awesome meme stock days of 2021. Which, as I mentioned earlier, could lead to the pot boiling over again.

I get it. The scars of crises past are still fresh. And rate cuts usually aren’t an immediate remedy.

But don’t freak out just yet.

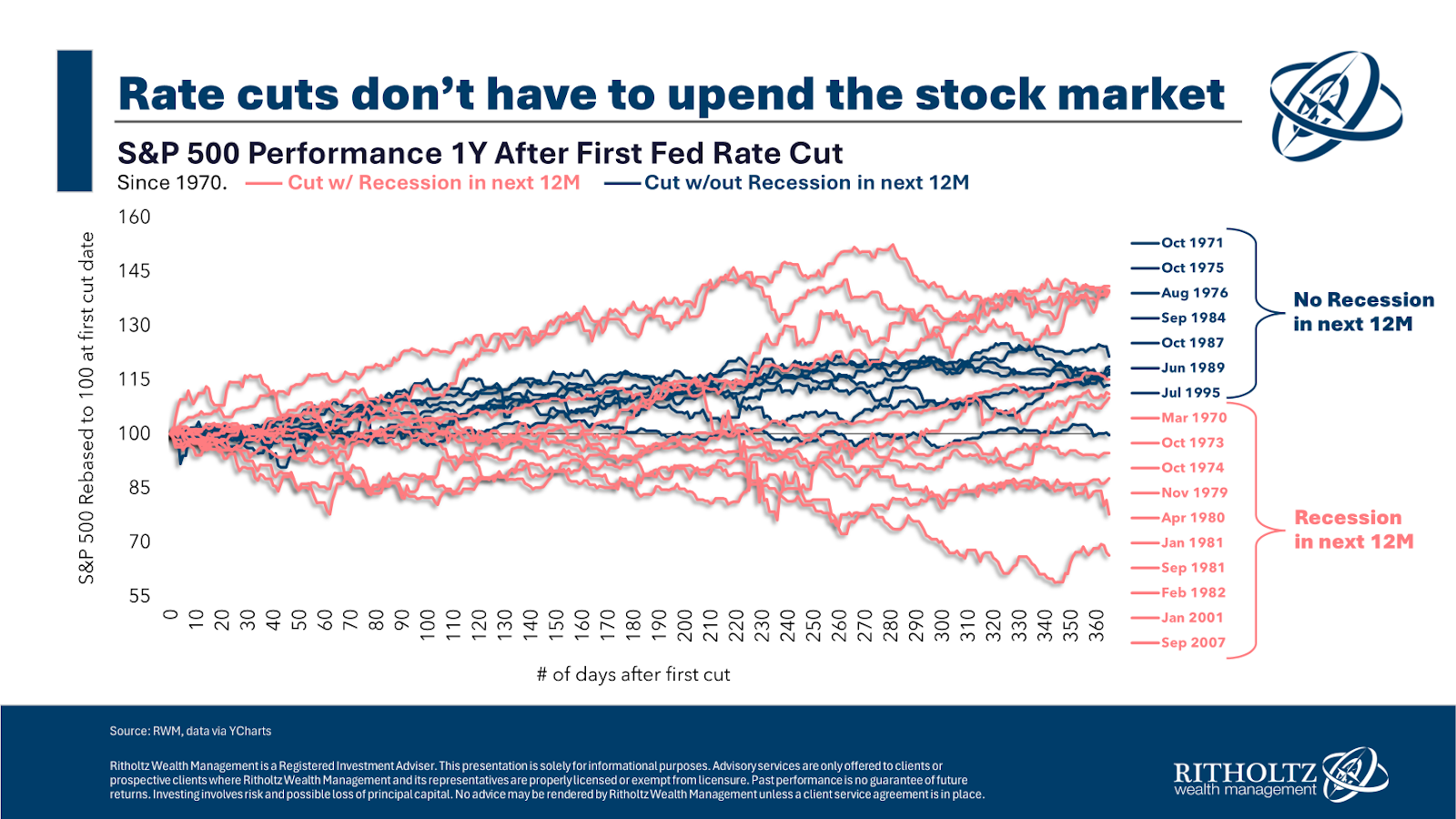

Reality may be somewhere in the middle of those two extremes. Here’s a great chart on the history of rate cuts from my colleague Matt C:

What you see above is how the stock market has performed during every rate cut cycle since 1970. There’s a lot of variability, but he highlighted one important distinction: rate cuts that happened during crisis (a recession) or celebration (no recession).

Right now, a good bit of Americans are employed and they’re spending money. It doesn’t look like we’re in a recession – or even close to one. If history proves correct, we could see the stock market continue to move higher in a slow, grinding fashion.

Rate cuts don’t always lead to financial irresponsibility. Nor do they always lead to a market crash.

Prepare for lower rates, but don’t get too carried away.

If you want more 🔥takes on rate cuts, listen to The Compound and Friends' conversation with Neil Dutta at RenMac (one of the smartest economists on the Street right now).

Thanks for reading!

Callie

Like what you just read? Share it with a friend, pretty please 😊