- OptimistiCallie

- Posts

- 🪂 Skydiving without a parachute

Hey hey, happy Monday.

Ah yes, the wild days are back. I’m not talking about the stock market, either. Yields are are taking center stage in this environment, and they’re challenging one of the key tenets of investing: that bonds will save you when stock prices are in freefall.

Not great. Let’s talk about it.

Smash the button below to share OptimistiCallie with a friend 😊

First, a confession.

I have never been skydiving.

I am not one of the 1% of Americans who have willingly jumped from a plane 10,000 feet in the air to chase a thrill, win a bet or get a sick mid-freefall selfie. If somebody asked me to go with a reputable instructor and offered me a few shots of tequila, I’d consider doing it.

Maybe. IDK. Ask me when I’m about to jump.

But when I try to think about the most stomach-turning, fear-inducing experience out there, skydiving always comes to mind. And yet, Americans skydived almost four million times in 2023 alone.

What keeps us flinging ourselves out of aircraft doors at cruising altitude? The parachute. A broad cloak of nylon that creates resistance against the air, slowing your fall and letting you glide down to the earth below. Without a parachute, skydiving is a death wish, not a recreational sport.

We skydive knowing we can lose everything if things go awry. Yet we do so because we crave what’s on the other side – glory, bragging rights, a rush – and we know we’re protected from catastrophic outcomes.

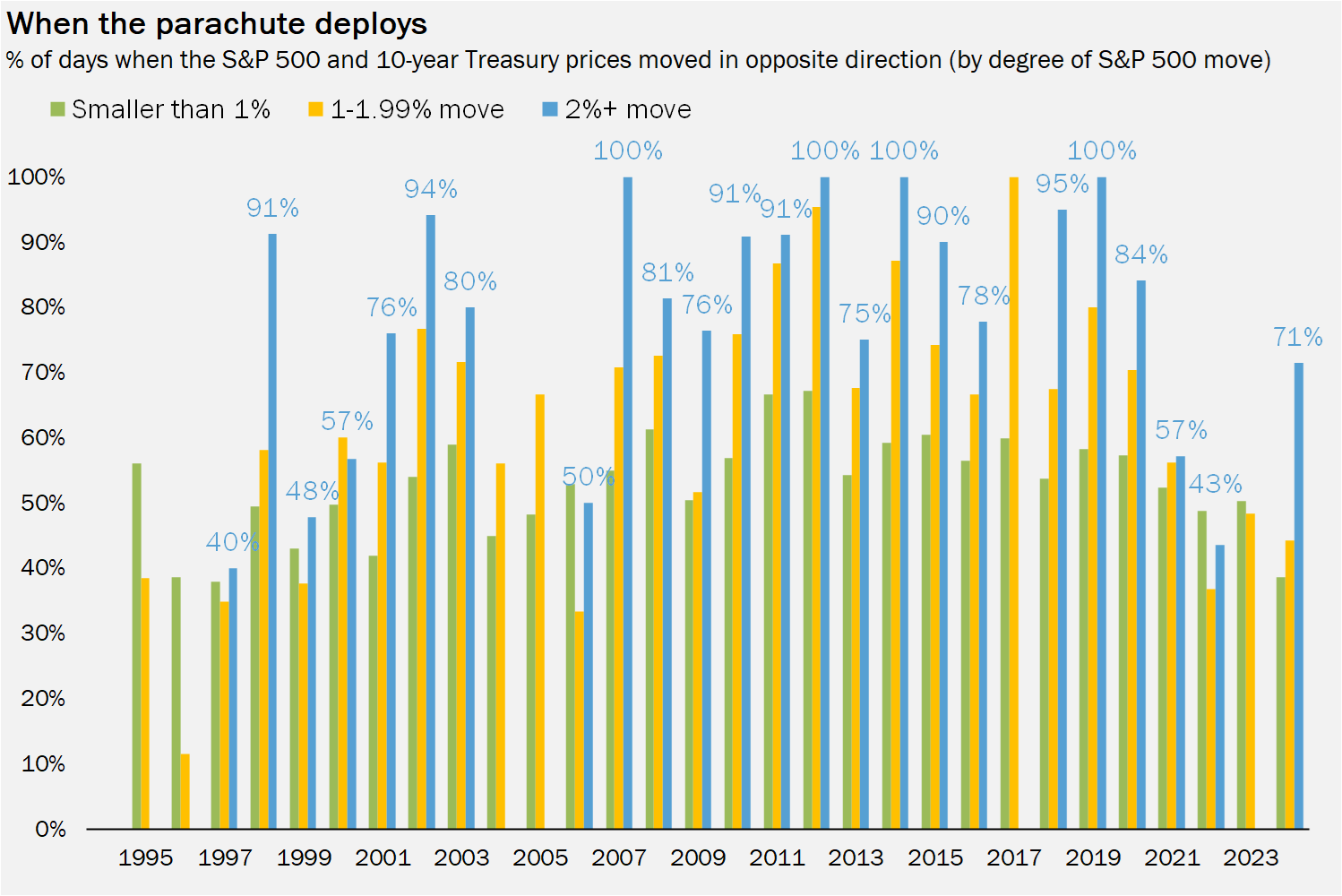

Investing in stocks may not be as risky as skydiving, but you could make the case that long-term government bonds are the portfolio equivalent of a parachute.

People tell you to buy long-term government bonds (Treasuries) because they often move opposite of stock prices, especially in times of turmoil.

Source: Callie Cox Media LLC, YCharts. The S&P 500 did not post any 2%+ days in 1995, 2004, 2005, and 2017.

That assumption has been tested recently, though. Bond parachutes haven’t deployed like they usually do as we forge deeper into an era of policy-fueled speculation.

And lately, they’ve left your portfolio in a terrifying spiral downwards.

To understand what I mean, you have to first understand what bonds are.

So here’s a primer on bonds, specifically Treasury bonds.

Skip if you’ve heard this before.

Government debt (or Treasuries) are the type of investment that people don’t think about until they matter. They’re these very unsexy I-owe-you agreements from the U.S. government to you that typically span anywhere from a month to 30 years. Bonds, in this context, are the catch-all term for Treasuries that mature in 10 years or more.

No thrill-seeking trader would ever venture into Treasuries, but many people don’t buy bonds for the thrill. Instead, they want stability. Predictability. A haven from the chaos, provided by one of the most risk-free investments you can get your hands on these days. After all, Uncle Sam has paid every single one of its creditors back.

Treasuries – like all other debt – also include a coupon payment for their gracious lenders. In the case of government bonds, the yield is a reflection of the growth and inflation expectations of the U.S. economy. Importantly, yields move in the opposite direction of bond prices.

TL;DR Treasury bonds are considered a classic parachute for your portfolio because they’re virtually risk-free. You receive interest payments for lending to Uncle Sam, and the market value of your bond can rise and fall over time.

Got it? Let’s go.

For decades, bond prices have followed a somewhat simple formula.

When people fear economic weakness, they buy bonds and sell stocks. When the economy is strong, they sell bonds and buy stocks.

Today? Not so much.

Bond prices have been in freefall these past few months, pushing yields to their highest levels in 17 years.

This isn’t exactly a product of a suddenly spectacular economic outlook, though. Since the beginning of December, about 70% of the 10-year yield’s rise has been attributed to the “other” category, or moves attributed to unusual forces like worries about long-term structural issues (like government debt), technical momentum, or just a plain ole lack of buyers.

Wall Street experts call this grab bag of reasons the “term premium”. Right now, the term premium baked into yields is at the highest since 2015, per Federal Reserve researchers:

Source: Callie Cox Media LLC; Bloomberg; Adrian, Crump, and Moench; Fed Bank of New York

In some ways, this makes sense. Conversations around here have shifted from concerns about a weak job market to discussions about tariffs and the $36 trillion in U.S. government debt. Inflation and the job market are still important, but the priorities are clear.

This isn’t particularly unusual, either. Every market is a tangled web of opinions. Some of those opinions just get a little louder at times, and you have to listen a little closer for the right clues.

On Wall Street, the term premium is mostly a wonky topic for bond experts to pontificate about.

But this is your parachute we’re talking about. It deserves more than just market theory and hand-waving.

When stocks fall because people lose faith in the economic outlook, we expect Treasuries to save us. But what if bond yields are jostled around by everything else outside of economic headlines? Can we still expect the parachute to deploy correctly?

Maybe not. Take the S&P 500’s 3% fall on December 18, after the Federal Reserve – that oh-so-cuddly group of policy nerds – told us the rate cuts may be ending soon.

If you panicked, you weren’t alone. One-day drops of 3% aren’t exactly normal. They’ve happened in less than 2% of days over the last three decades. It’s not quite the thrill of skydiving, but you get the idea. On days like those, every tick down could mean the difference between holding and running for the hills.

Our parachutes didn’t deploy, either. Treasury prices actually fell 0.6% on the day, leading to a total fall of 3.5% in an equal-weighted stock and bond portfolio. What was the 112st day in the stock market over a three-decade span turned into the 50th worst day when you account for the decline in Treasuries.

Same thing happened this past Friday. The December jobs report showed hiring is strong and unemployment dropped. Good news all around! Yet the S&P 500 dropped 1.5%, and Treasuries fell 0.5%. Granted, the rise in yields (and drop in prices) that day was more due to inflation, but recent failures have forced people to think twice about the reliability of their parachutes.

Some of us are getting flashbacks to 2022, the third-worst year for a stock and bond portfolio in history (according to my fabulous colleague Ben Carlson). I wouldn’t go there just yet. Stocks have a better foundation under them, and inflation isn’t scorching hot. Narratives change quickly these days, too. Sure, the economy seems fine for now, but one bad jobs report could push growth concerns back to the forefront.

So what can you do? Just stop skydiving – or investing – altogether?

Nah. You can’t give up risk entirely. The world doesn’t work like that.

For now, I’d be extra careful about how you react to day-to-day moves. Expect yields to be more of a plaything for politicians, deficit doomers and Fed nerds at these levels. Think about buying a back-up parachute for your portfolio. Maybe shorter-term debt and cash.

It’s not all bad. Enjoy the high yields. Clip those coupons. Steer clear of those 7% mortgage rates, oof.

Most importantly, remember that we’re living in a galaxy-braining period on Wall Street in which traditional assumptions don’t always apply. Some days are just going to feel like you’re jumping out of a plane and crossing your fingers.

In times like these, you can’t always rely on your portfolio to save you. Emergency funds are extra important, and airtight goals with clear targets are your lifeline.

Thanks for reading!

Callie

Like what you just read? Share it with a friend, pretty please 😊